Introduction of SECR

SECR was launched on April 1st, 2019. Large firms, including nonprofit organizations, are required by the UK government to submit annual reports detailing their energy and carbon emissions as well as any efficiency initiatives they’ve undertaken and Streamlined Energy and Carbon Reporting (SECR) coincides with the end of the Carbon Reduction Commitment (CRC) Energy Efficiency Scheme.

Meaning of SECR

The SECR is legislation mandating that large businesses and organizations must report their energy and carbon emissions – along with any efficiency measures taken throughout the year – on an annual basis.

Objectives of SECR

- Identifying low-cost or no-cost efficiency opportunities.

- Boosting green and sustainability credentials.

- Tracking environmental KPIs year on year.

- Highlighting risks from volatile energy and commodity prices.

- Delivering improved environmental disclosures.

Why has SECR been introduced?

- SECR aims to make carbon and energy reporting advantages available to more companies.

- To require companies to disclose their energy and carbon usage is consistent with the Task Force on Climate-related Financial Disclosures of the G20 Financial Stability Board because it gives investors and other financial actors crucial knowledge to aid in the transition to a sustainable, low-carbon economy.

- The SECR builds on, but does not replace, existing schemes such as the mandatory greenhouse gas (GHG) reporting, the Energy Saving Opportunity Scheme (ESOS), and the Climate Change Agreements (CCA) Scheme.

Who needs to comply ?

-

- Over 11,900 UK organizations are required to comply with SECR regulations.

- Quoted companies of any size that are already obliged to report under mandatory greenhouse gas reporting regulations.

- Unquoted companies incorporated in the UK which meet the definition of ‘large’ under the Companies Act 2006.

- ‘Large’ Limited Liability Partnerships (LLPs).

Large is determined if it meets two of the following three criteria:

- Annual balance sheet of over £18m

- Annual turnover of more than £36m

- > 250 employees

Where does it need to comply?

- If companies report at a group level, the thresholds should consider these figures at aggregate level, including subsidiaries.

- In assessing whether the 40,000 kWh threshold is met, companies must consider, as a minimum, all the energy from gas, electricity and transport fuel usage.

- Where a large company does not consume more than 40,000 kWh of energy in a reporting period, it qualifies as a low energy user and is exempt from reporting under these regulations.

Exemption for companies from SECR

- Not registered in the UK.

- UK subsidiaries that qualify for SECR but are already covered by a parent’s group report (unless the parent company is not registered in the UK).

- Public sector organizations, charities and private sector organizations that don’t file reports to Companies House.

- Companies that use less than 40,000 kWh of energy in the reporting year.

How does SECR work for group and subsidiary-level reporting?

- Sometimes a report at the group level is necessary. Data on energy consumption and carbon emissions for the main company and all subsidiaries should be included in a group-level report.

- A subsidiary that would not otherwise be compelled to report under SECR independently from the group may delete its energy and carbon details in the group report.

- When subsidiary companies subject to SECR have already reported their energy and carbon information in a parent’s group-level report, filing a separate energy and carbon report isn’t necessary.

SECR principles for accounting and reporting environmental impacts

- Relevant and serves the decision making needs of users.

- Quantitative, measurable and accompanied by a narrative.

- Accurate to reduce uncertainties and boost confidence in users.

- Complete and include all information within the reporting boundary.

- Consistent methodology throughout the while noting any changes to data.

- Comparable by using accepted key performance indicators(KPI’s).

- Transparent in every aspect of the report.

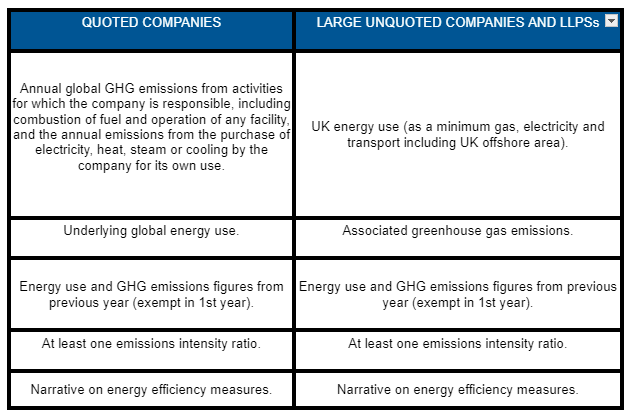

What SECR information needs to be reported ?

The reporting requirements differ for each business

What Are SECR Reporting Requirements?

- Energy use, including gas, purchased electricity, and transport fuel.

- GHG emissions reported in tonnes of carbon dioxide equivalent (CO2e).

- Methodology used to make calculations for emissions and energy use.

- At least one intensity ratio comparing emissions to a business metric.

- A narrative description of efforts taken to improve the company’s energy efficiency during the financial year.

Previous years’ figures for GHG emissions and energy use.

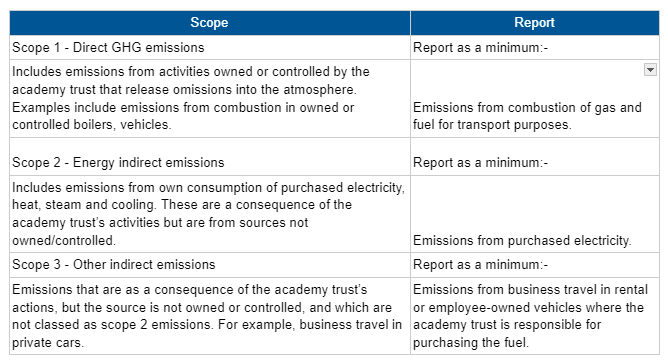

Emission scopes and their minimum reporting requirements

How Can Businesses Improve SECR Reporting and Compliance?

- Staff training and education can help team members get aligned and informed on how and why they need to assist with SECR reporting. Explaining what type of information, where it comes from, and who’s responsible for collecting are a few things businesses can do to help their team get started.

- Implementing methods to measure and analyze emissions and energy can help streamline the process. SECR reporting may include trial and error before finding the best process.

Using a comprehensive tool like CMAPs can automate the tedious aspects of sustainability disclosure and information requests.